Loan Programs

Selecting the ideal mortgage depends on your unique credit profile, down payment, and long-term financial goals. During our initial consultation, I will evaluate these factors to help you identify the most advantageous loan program for your specific situation.

Conventional Loans

Conventional loans offer competitive rates and flexible terms without government backing, allowing for more lender-specific customization. Please provide your details so we can determine if this mortgage type aligns with your financial goals.

Who It's Best For

Buyers with solid credit (typically 620+), stable income, and the ability to make at least a small down payment.

Key Features

Down payments as low as 3% for qualified first-time buyers

Competitive interest rates, especially for higher credit scores

Private mortgage insurance (PMI) required if down payment is below 20%, but can be removed later

Fixed-rate and adjustable-rate options available

Can be used for primary residences, second homes, and investment properties

Things to Consider

Conventional loans have stricter credit and income requirements than FHA loans. If your credit is on the lower end or your financial situation is more complex, we have other options that we can explore.

FHA Loans

FHA loans are government-backed mortgages designed with flexible qualification requirements to increase homeownership accessibility. Contact me to discuss the program’s trade-offs and determine if this is the most strategic financing option for your needs.

Who It's Best For

First-time buyers, buyers with lower credit scores, or anyone who needs a lower down payment option.

Key Features

Down payment as low as 3.5%

Credit scores as low as 580 (and sometimes lower with a larger down payment)

More forgiving of past credit issues like bankruptcy or foreclosure

Can be used for primary residences

Things to Consider

FHA loans require mortgage insurance for the life of the loan in most cases, which adds to your monthly payment. They also have property condition requirements, so the home must meet certain standards.

VA Loans

As a veteran specializing in VA loans, I am dedicated to helping fellow service members maximize the superior mortgage benefits they have earned. Let’s discuss your eligibility and the application process to determine if this specialized program is your best path to homeownership.

Who It's Best For

Veterans, active-duty military, National Guard and Reserve members with qualifying service, and eligible surviving spouses.

Key Features

No down payment required in most cases

No private mortgage insurance (PMI)

Competitive interest rates

Flexible credit guidelines

Limits on closing costs

Things to Consider

VA loans require a Certificate of Eligibility (COE), which I can often pull for you electronically. There's also a funding fee that varies based on your service history and down payment, though some borrowers are exempt.

Jumbo Loans

Jumbo loans provide high-balance financing for luxury properties exceeding the 2026 conforming limit of $832,750. Contact me to explore competitive jumbo options and determine the most effective structure for your high-value home purchase.

Who It's Best For

Buyers purchasing higher-priced homes who need to borrow more than conforming loan limits allow.

Key Features

Loan amounts above conforming limits

Competitive rates for well-qualified borrowers

Fixed-rate and adjustable-rate options

Can be used for primary residences, second homes, and investment properties

Things to Consider

Jumbo loans typically require stronger credit (often 700+), larger down payments (usually 10-20%), and more significant cash reserves. Underwriting is also more thorough.

Investor and DSCR Loans

Debt Service Coverage Ratio (DSCR) loans streamline portfolio expansion by qualifying properties based on rental income rather than personal debt-to-income ratios. Contact me to explore how these investor-focused products can optimize your financing strategy and accelerate your real estate growth.

Who It's Best For

Real estate investors who want to scale their portfolio without relying on personal income documentation.

Key Features

Qualification based on property income, not personal income

No tax returns or W-2s required

Works for single-family rentals, multi-family properties, and short-term rentals

Can close in an LLC for liability protection

No limit on number of properties

Things to Consider

DSCR loans typically require a larger down payment (usually 20-25%) and have slightly higher rates than conventional loans. The property must generate enough income to cover the debt payment, typically a DSCR of 1.0 or higher.

Refinance Options

Strategic refinancing can optimize your financial position by lowering monthly payments, shortening loan terms, or accessing home equity. Contact me to review your goals and run a detailed cost-benefit analysis to determine if the current market favors your situation.

Rate-and-Term Refinance

Replace your current loan with a new one at a better rate, different term, or both. You're not taking cash out, just restructuring for improved terms.

Cash-Out Refinance

Borrow more than your current loan balance and receive the difference as cash. Commonly used for home improvements, debt consolidation, or major expenses.

FHA Streamline Refinance

For current FHA loan holders. A simplified process with less documentation, designed to make refinancing easier.

VA Interest Rate Reduction Refinance Loan (IRRRL)

For veterans with existing VA loans. Also called a VA Streamline, this program allows you to refinance with minimal paperwork and often no appraisal.

Find the Right Loan for Your Situation

These are general guidelines. Your specific situation may vary. Reach out and I'll help you understand what applies to you.

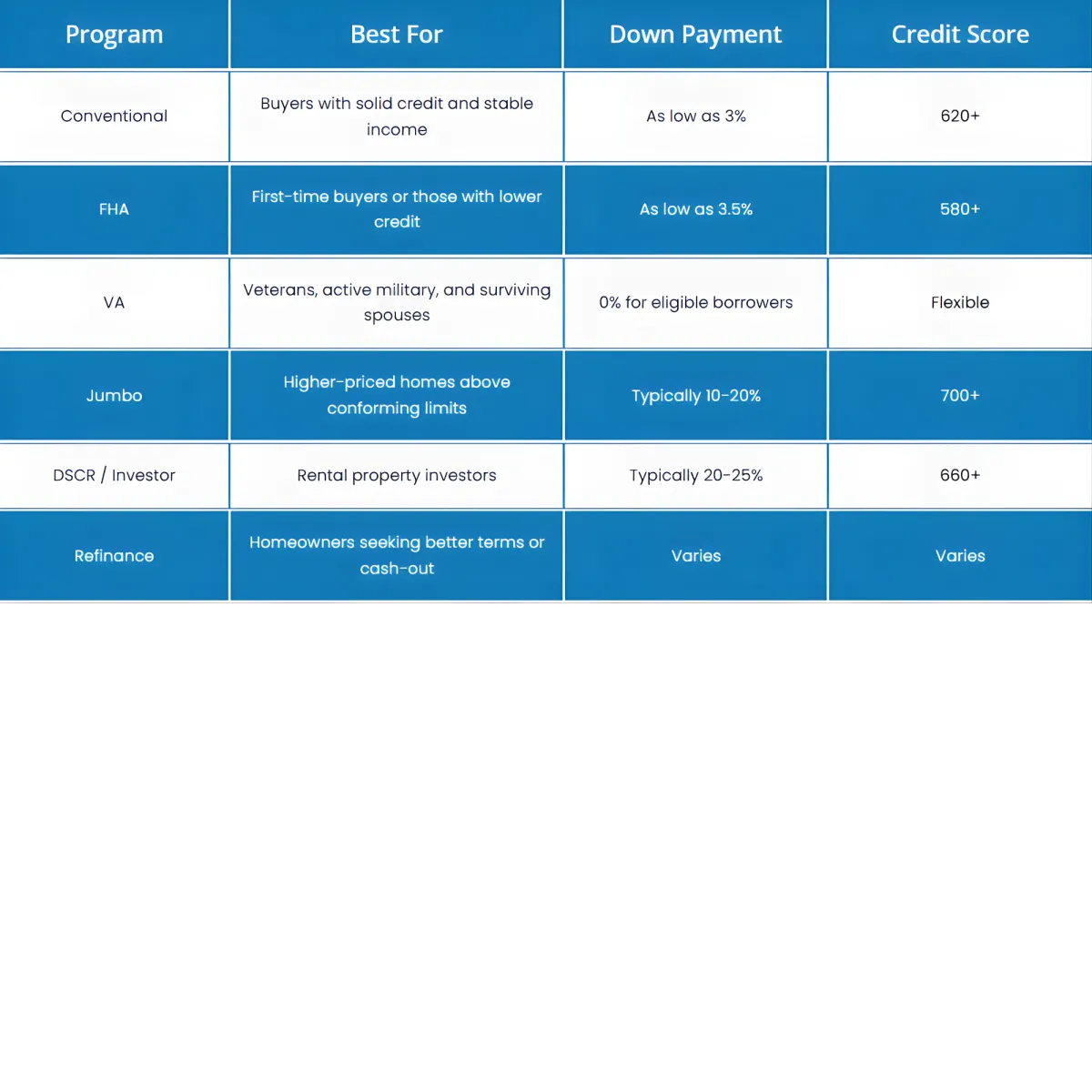

Program

Best For

Down Payment

Credit Score

Conventional

Buyers with solid credit and stable income

As low as 3%

620+

FHA

First-time buyers or those with lower credit

As low as 3.5%

580+

VA

Veterans, active military, and surviving spouses

0% for eligible borrowers

Flexible

Jumbo

Higher-priced homes above conforming limits

Typically 10-20%

700+

DSCR / Investor

Rental property investors

Typically 20-25%

660+

Refinance

Homeowners seeking better terms or cash-out

Varies

Varies

Find the Right Loan for Your Situation

These are general guidelines. Your specific situation may vary. Reach out and I'll help you understand what applies to you.

Not Sure Which Program Is

Right for You?

Selecting the optimal mortgage program can be complex, and my role is to simplify that process through personalized guidance. Let’s have a brief conversation to review your financial goals and identify the most advantageous options without unnecessary jargon or pressure.

A few questions we'll cover:

Are you buying or refinancing?

Is this a primary residence or investment property?

Are you self-employed or W-2 employed?

How much do you have available for a down payment?

Are you a veteran or currently serving in the military?

What's your approximate credit score range?

You don't need all the answers right now. We'll figure it out together.

Call/Text: 512-293-8890

Email: [email protected]

Ready to Get Started?

The first step is simple: a conversation. We'll talk about your goals, We'll answer your questions, and we'll figure out the best path forward. No obligation. No pressure. Just honest guidance.

Call/Text: 512-293-8890

Email: [email protected]

Transparency

Clear, honest guidance.

Expertise

Specialized industry knowledge.

Accessibility

Simple solutions for everyone.

Equal Housing Lender

Gary Caples (NMLS #251360) | Prodigy Mortgage

(NMLS #237857) | Licensed in Texas

This is not a commitment to lend. All loans are subject to credit approval. Programs, rates, terms, and conditions are subject to

change without notice. Other restrictions may apply.

COMPANY

SERVICES

LEGAL

FOLLOW US

Copyright 2026. Gary Caples. All Rights Reserved.