VA Home Loans

in Austin, TX

As a fellow veteran and Texas-licensed loan officer, I specialize in helping service members maximize their VA home loan benefits to achieve $0$ down payments and competitive rates. I am committed to providing the expert guidance necessary to ensure you successfully navigate this program and secure the home you’ve earned.

The VA Loan Advantage

VA loans aren't just another mortgage option. For eligible borrowers, they're often the best option available. Here's why:

No Down Payment Required

Most VA loans allow you to finance 100% of the home's value. You can buy a home without putting any money down, keeping your savings intact for moving expenses, furniture, or reserves.

No Private Mortgage Insurance (PMI)

Unlike conventional and FHA loans, VA loans don't require monthly mortgage insurance, even with zero down payment. This can save you hundreds of dollars every month compared to other loan types.

Competitive Interest Rates

Because VA loans are partially guaranteed by the government, lenders can offer rates that are often lower than conventional loans. Over the life of your mortgage, this can add up to significant savings.

Flexible Credit Guidelines

VA loans tend to be more forgiving of past credit challenges than conventional loans. If your score isn't perfect or you've had some bumps in the road, you may still qualify.

Limits on Closing Costs

The VA limits what veterans can be charged for certain closing costs, adding another layer of protection and keeping more money in your pocket.

A Benefit You Can Use Again

Your VA loan eligibility isn't one-and-done. You can use it multiple times throughout your life: to buy, refinance, or purchase again after selling a previous home.

VA Loan Eligibility

VA loans are available to those who have served our country. You may be eligible if you're:

A veteran who served on active duty and was discharged under conditions other than dishonorable

An active-duty service member currently serving

A member of the National Guard or Reserves with qualifying service

A surviving spouse of a veteran who died in service or from a service-connected disability (in certain cases)

Minimum Service Requirements

Service requirements vary based on when and how you served. General guidelines include:

Wartime service: 90 consecutive days of active duty

Peacetime service: 181 consecutive days of active duty

National Guard/Reserves: 6 years of service, or 90 days under Title 10 orders

These are general guidelines. Eligibility can depend on your specific service dates and circumstances. If you're not sure whether you qualify, reach out. I can often pull your Certificate of Eligibility (COE) electronically and confirm your status within minutes.

The Certificate of Eligibility (COE)

To use your VA loan benefit, we need to confirm your eligibility with a Certificate of Eligibility, or COE. This document shows lenders that you meet the service requirements for a VA loan.

How to Get Your COE?

In most cases, I can pull your COE electronically through the VA's system. It often takes just a few minutes. If your records aren't available electronically, we can request it manually using your DD-214 or other discharge documents.

Don't have your DD-214 handy? Don't worry. We'll figure it out together. Reach out and I'll walk you through the process.

Understanding the VA Funding Fee

VA loans don't require PMI, but there is a one-time funding fee that helps keep the VA loan program running for future veterans. This fee varies based on a few factors.

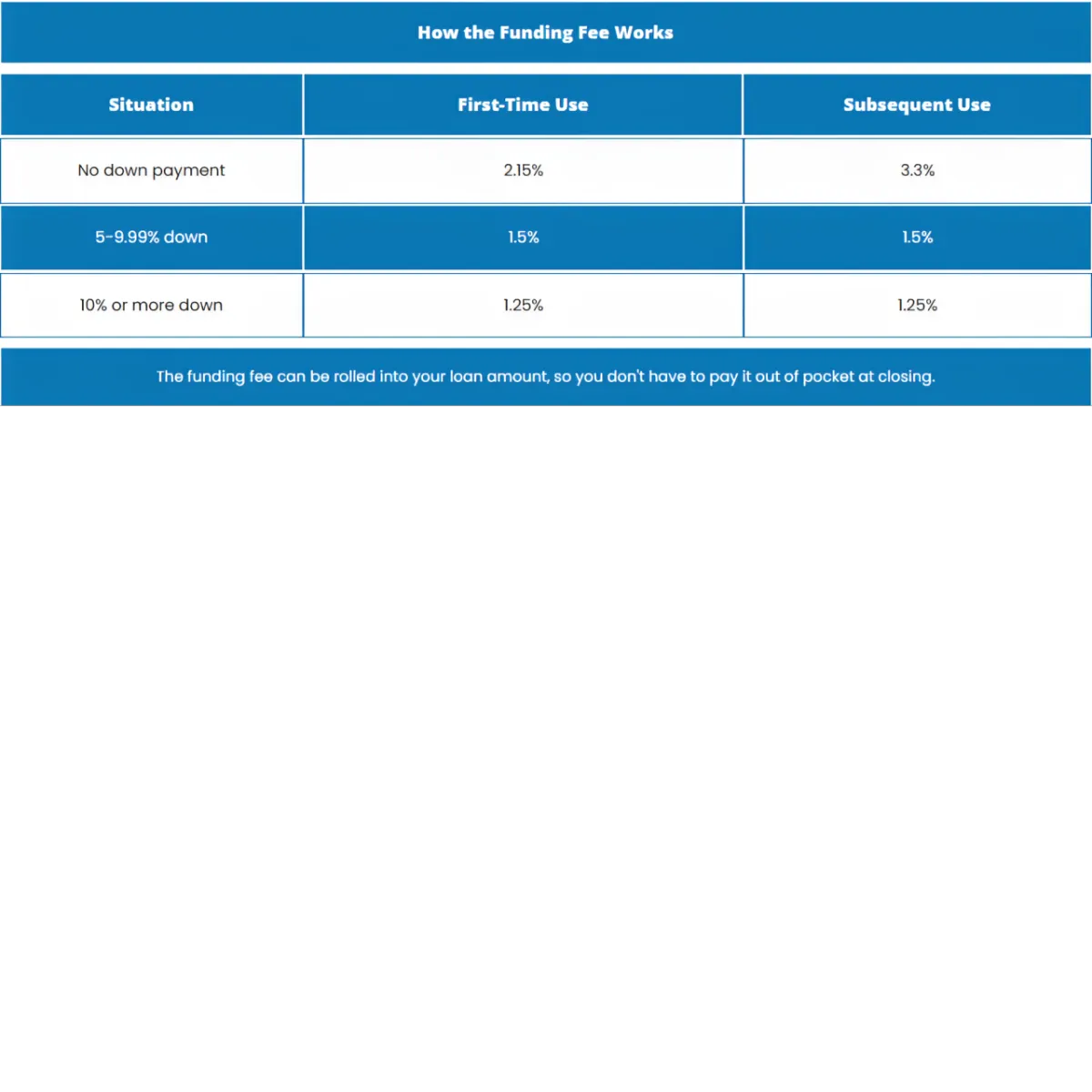

How the Funding Fee Works

Situation

First-Time Use

Subsequent Use

No down payment

2.15%

3.3%

5-9.99% down

1.5%

1.5%

10% or more down

1.25%

1.25%

The funding fee can be rolled into your loan amount, so you don't have to pay it out of pocket at closing.

Exemptions

Some veterans are exempt from the funding fee entirely, including:

Veterans receiving VA disability compensation

Veterans entitled to receive VA disability compensation but receiving retirement or activeduty pay instead

Surviving spouses of veterans who died in service or from a service-connected disability

Active-duty service members who provide evidence of receiving the Purple Heart

Not sure if you're exempt? Let's talk. I'll help you understand what applies to your situation.

Understanding the VA Funding Fee

VA loans don't require PMI, but there is a one-time funding fee that helps keep the VA loan program running for future veterans. This fee varies based on a few factors.

Exemptions

Some veterans are exempt from the funding fee entirely, including:

Veterans receiving VA disability compensation

Veterans entitled to receive VA disability compensation but receiving retirement or activeduty pay instead

Surviving spouses of veterans who died in service or from a service-connected disability

Active-duty service members who provide evidence of receiving the Purple Heart

Not sure if you're exempt? Let's talk. I'll help you understand what applies to your situation.

What Else You Should Know

VA Loan

Limits

Veterans with full entitlement face no loan limits as of 2020, allowing borrowing of any lender-approved amount based on personal income and credit.

If you have remaining entitlement from a previous VA loan that hasn't been restored, limits may apply. We'll review your specific situation together.

Property Requirements

VA loans require Minimum Property Requirements to ensure homes are safe, structurally sound, and sanitary, protecting you from purchasing properties with hidden issues.

The VA appraisal process checks for these requirements. If issues come up, we'll discuss your options.

Occupancy Requirement

VA loans are for primary residences. You must intend to live in the home. Investment properties or vacation homes require different loan products.

If you're looking to purchase a rental property, I have investor-focused options available too.

How We'll Get You Into Your Home

Step 1: Confirm Eligibility and Get Pre-Approved

We'll start with a conversation about your goals and timeline. I'll pull your COE (often instantly) and review your finances to issue a pre-approval. You'll know your buying power and be ready to shop with confidence.

Step 2: Find Your Home

Work with your real estate agent to find a home that fits your needs and budget. Your pre-approval letter shows sellers you're a serious, qualified buyer

Need an agent recommendation? I'm happy to connect you with agents I trust who have experience working with VA buyers.

Step 3: Contract, Appraisal, and Underwriting

Once you're under contract, I'll order the VA appraisal, which confirms the home's value and checks for Minimum Property Requirements. Your file will move through underwriting, and I'll keep you updated every step of the way.

Step 4: Close and Get Your Keys

Sign the final documents, the loan funds, and you're officially a homeowner. The VA loan program has helped millions of veterans achieve this moment. I'll make sure you get there too.

How We'll Get You Into Your Home

Step 1: Confirm Eligibility and Get Pre-Approved

We'll start with a conversation about your goals and timeline. I'll pull your COE (often instantly) and review your finances to issue a pre-approval. You'll know your buying power and be ready to shop with confidence.

Step 2: Find Your Home

Work with your real estate agent to find a home that fits your needs and budget. Your pre-approval letter shows sellers you're a serious, qualified buyer

Need an agent recommendation? I'm happy to connect you with agents I trust who have experience working with VA buyers.

Step 3: Contract, Appraisal, and Underwriting

Once you're under contract, I'll order the VA appraisal, which confirms the home's value and checks for Minimum Property Requirements. Your file will move through underwriting, and I'll keep you updated every step of the way.

Step 4: Close and Get Your Keys

Sign the final documents, the loan funds, and you're officially a homeowner. The VA loan program has helped millions of veterans achieve this moment. I'll make sure you get there too.

Already Have a VA Loan?

If you currently have a VA loan, you have options to refinance and potentially improve your situation.

VA Interest Rate Reduction Refinance Loan (IRRRL)

Also called a VA Streamline Refinance, the IRRRL makes it easy to refinance your existing VA loan to a lower interest rate. Benefits include:

Minimal documentation required

No appraisal in most cases

No out-of-pocket costs (closing costs can be rolled into the loan)

Quick closing timeline

VA Cash-Out Refinance

Need to access your home's equity? A VA cash-out refinance allows you to borrow against your equity, up to 100% of your home's value in many cases. Common uses include home improvements, debt consolidation, or other major expenses.

Considering a refinance? Let's run the numbers together and see if it makes sense for you.

A Fellow Veteran Who Knows

VA Loans

Not every lender understands VA loans. Some avoid them because they require more expertise to process correctly. I lean into them.

As a veteran myself, I take pride in helping fellow service members use the benefit they've earned. I know the program inside and out: the funding fee calculations, the COE process, the appraisal requirements, and how to structure deals that work.

What You Get When You Work With Me

Fast COE retrieval, often electronic and same-day

Clear explanation of how the VA program works for your specific situation

Pre-approval that sellers take seriously

Proactive communication throughout the process

A smooth closing with no surprises

VA Loan Questions I Hear Often

Can I use my VA benefit more than once?

Yes. Your VA entitlement can be restored after you pay off a VA loan. In some cases, you can even have more than one VA loan at a time. Let's talk through your situation and I'll help you understand your options.

What credit score do I need for a VA loan?

The VA doesn't set a minimum credit score, but lenders do. Generally, a 580-620+ score is needed. Even if your credit isn't perfect, reach out. We may have options.

Can I buy a condo with a VA loan?

Yes, but the condo complex must be on the VA's approved list. If it's not currently approved, we can sometimes get approval. Let me know what property you're looking at and I'll help you figure it out.

What if I have a bankruptcy or foreclosure in my past?

You may still qualify. The VA program is generally more flexible than conventional loans.

We'll look at your specific timeline and circumstances together.

I'm currently serving overseas. Can I still buy?

Yes. We can work through the process remotely. Power of attorney arrangements can be set up if needed for closing. Reach out and we'll coordinate the details.

Can my spouse's income be included?

Yes, if they'll be on the loan. Non-borrowing spouse income can sometimes be considered for residual income requirements as well. We'll review your specific situation.

I'm not sure if I'm eligible. Should I still reach out?

Absolutely. I can often pull your COE in minutes and give you a definitive answer.

There's no cost or obligation to find out.

What Clients Say

Don't Just Take My Word For It

When applying for a home loan it's a time consuming and stressful ordeal - but having "Supreme Lending" and "Loan Officer - Gary Caples" on your side really can make the process a much easier and less stressful business transaction.

Carl and April Kearney

Gary Caples, My Mortgage Consultant was very patient and tireless in his mission to get my loan underway. Always there to answer a question and kept me informed about the process and the timelines.

Jeremy Johnson

“After moving to Austin from Los Angles, we were job hunting and planning to get married. During a very stressful time in our lives, Gary’s expertise, hard work and patience with us made our home buying experience very smooth and positive.”

Andy Molloy

Ready to Get Started?

The first step is simple: a conversation. We'll talk about your goals, We'll answer your questions, and we'll figure out the best path forward. No obligation. No pressure. Just honest guidance.

Call/Text: 512-293-8890

Email: [email protected]

Proudly Serving Austin and

Central Texas

I work with buyers and homeowners across the Austin metro area and

assist with buying or refinancing anywhere in Texas—let’s talk.

Transparency

Clear, honest guidance.

Expertise

Specialized industry knowledge.

Accessibility

Simple solutions for everyone.

Equal Housing Lender

Gary Caples (NMLS #251360) | Prodigy Mortgage

(NMLS #237857) | Licensed in Texas

This is not a commitment to lend. All loans are subject to credit approval. Programs, rates, terms, and conditions are subject to

change without notice. Other restrictions may apply.

COMPANY

SERVICES

LEGAL

FOLLOW US

Copyright 2026. Gary Caples. All Rights Reserved.